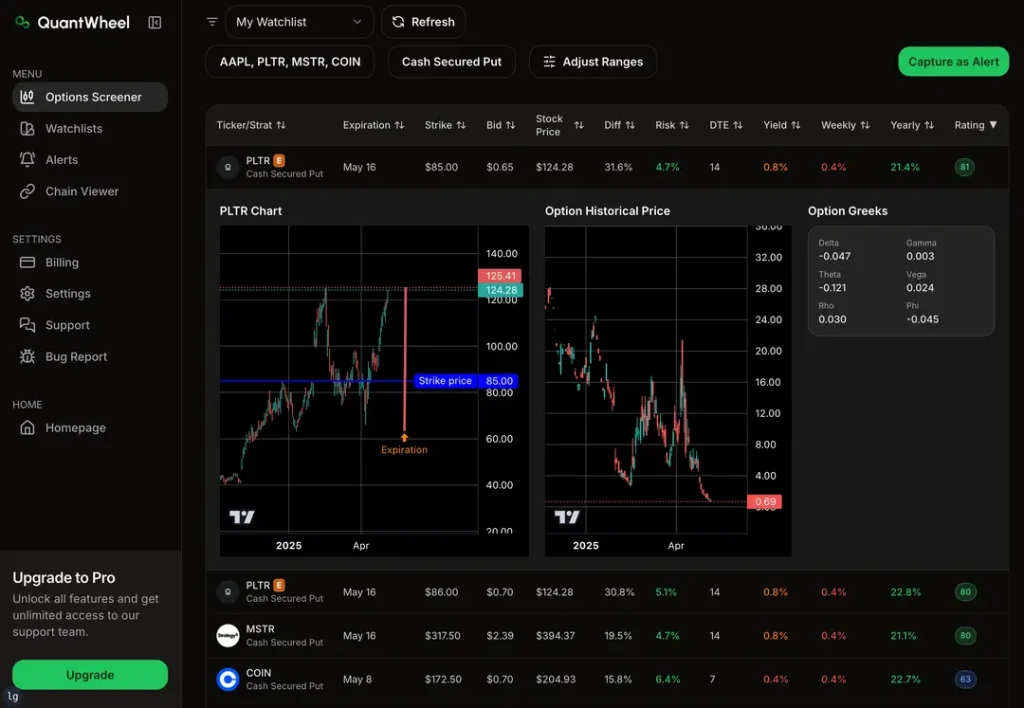

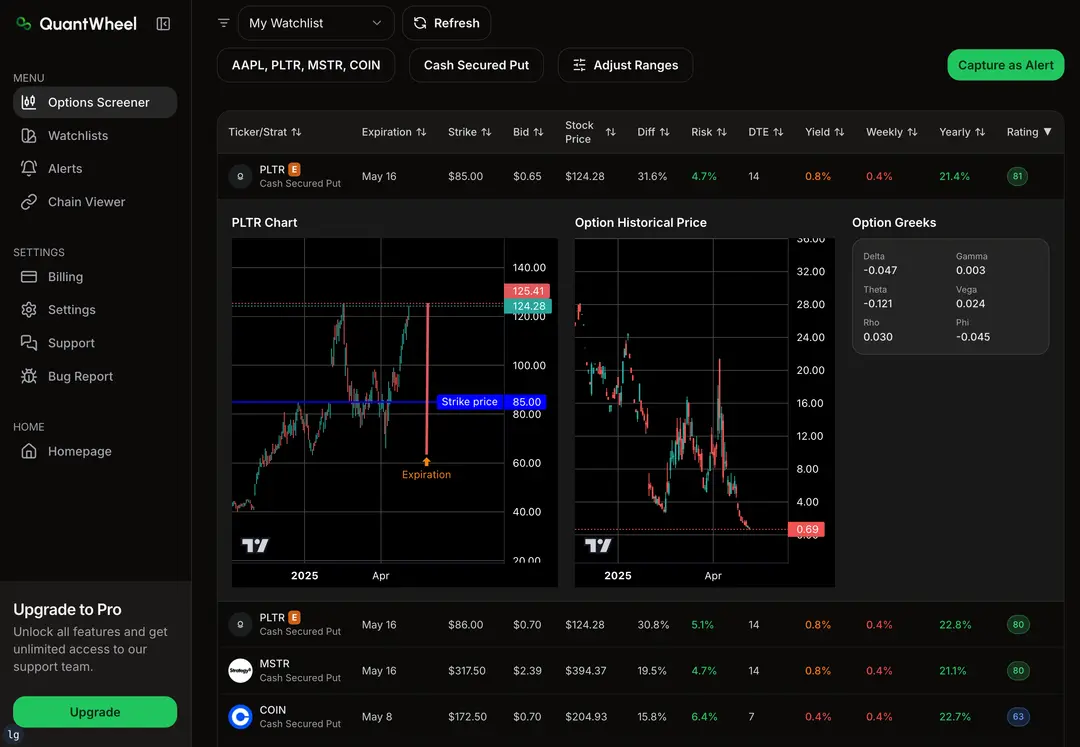

Options Greeks measure how different factors affect the price of options. They help you understand how changes in things like the underlying asset’s price, time, and market volatility can impact your option’s value. Knowing these Greeks lets you make smarter choices when trading options.

Each Greek focuses on a specific risk or reward element. For example, Delta shows how much an option’s price moves with the stock, while Theta measures how time passing affects its value. By learning these, you can better predict how your options will behave.

Using Greeks can give you an edge as an investor or trader by helping you manage your risks and spot opportunities more clearly. This guide will break down the key Greeks in a simple way so you can use them confidently.

Understanding Options Greeks

Options Greeks help you measure how changes in market factors affect the price and risk of your options contracts. They are key tools to analyze exposure, manage risk, and improve your trading strategies. You will learn what Greeks are, how they impact pricing, and why they matter for your option positions.

Definition and Purpose of Greeks

Greeks are mathematical values that show how sensitive your options are to different factors. Each Greek represents a specific type of risk or sensitivity. For example, Delta measures how much the option’s price moves when the underlying asset’s price changes.

The main Greeks include Delta, Gamma, Theta, Vega, and Rho. You use these to understand potential profit or loss in your position. They guide you in managing risk and adjusting your portfolio to changing market conditions.

Role in Options Pricing and Risk Management

Greeks are vital in pricing options because they break down complex risk into simpler parts. Pricing models use Greeks to estimate how likely your option will gain or lose value. This allows you to calculate the option’s premium based on market factors like price and volatility.

For risk management, Greeks help you spot where your portfolio is exposed. For example, a high Theta means the option loses value quickly as time passes, so you might adjust your position to reduce loss. This lets you defend against unexpected market moves.

Sensitivity to Underlying Asset Changes

Each Greek responds to different changes in the market. Delta shows sensitivity to the underlying asset price. Gamma tells you how Delta changes when the price moves, helping you predict future risks.

Vega measures sensitivity to volatility, showing how option value reacts to market uncertainty. Theta shows time decay, or how option value drops as expiration nears. Rho measures response to interest rate changes, which is less impactful but still relevant in some cases.

Impact on Option Trading Strategies

Understanding Greeks lets you build smarter trading strategies. If you want stable income, focus on Theta to capture time decay. If you expect strong price moves, Delta and Gamma guide your choice of strike prices and position size.

Vega is key when volatility is high or expected to change. You might buy options to benefit from rising volatility or sell them to profit from falling volatility. Using Greeks also helps balance your portfolio’s overall risk by spreading exposure across different positions.

In-Depth Breakdown of Major Greeks

Understanding how option prices move helps you manage risk and make better trades. You need to know how price, time, volatility, and interest rates affect your option’s value.

Delta: Measuring Price Sensitivity

Delta shows you how much the option’s price will change when the stock price moves by $1. For call options, delta ranges from 0 to 1. For put options, it ranges from 0 to -1. If a call option has a delta of 0.6, its price will rise by about $0.60 if the stock price goes up by $1.

Delta also reflects the chance an option will expire in the money. Higher delta means higher probability. If you buy calls, you want a positive delta to gain when the stock rises.

Delta changes as the stock price moves. This is why tracking delta helps you understand your option’s sensitivity to the underlying security.

Gamma: Rate of Change of Delta

Gamma tells you how fast delta changes when the stock price moves. Higher gamma means delta will change quickly, making your option’s price more sensitive to stock moves.

Gamma is highest when the stock price is near the option’s strike price. It is lower when the option is deep in or out of the money.

You pay attention to gamma if you manage risk actively. It helps you predict how your position reacts to large price moves. For option buyers, high gamma can increase profit potential but also adds risk because delta shifts faster.

Theta: The Effect of Time Decay

Theta measures how much value your option loses as time passes, assuming everything else stays the same. This loss is called time decay.

Options lose value faster as expiration approaches. Theta is usually negative for option buyers because time decay works against them. Sellers benefit from theta since they keep the premium as time passes.

Time decay hits out-of-the-money options harder since their chance to expire in the money shrinks over time. You must factor in theta when choosing when to buy or sell to avoid losing value for no reason.

Vega: Sensitivity to Volatility

Vega tells you how much your option’s price changes when market volatility shifts by 1%. If volatility rises, option prices usually go up, because higher volatility increases the chance of big price moves.

You want higher vega if you expect more market swings. Vega is highest for at-the-money options with long expiration dates.

When volatility falls, vega causes your option’s price to drop. Option buyers face risks here, while sellers might benefit. Knowing vega helps you evaluate how changes in market conditions affect your option’s value.

Rho: Impact of Interest Rates

Rho shows you how much your option’s price changes when interest rates move by 1%. Interest rates affect the cost of carrying a position and the present value of the strike price.

For call options, higher rates usually increase the option’s value. For puts, higher rates decrease it. However, rho’s effect tends to be smaller compared to other Greeks.

Rho becomes more important for options with longer times until expiration. When interest rates change, you can use rho to adjust your strategy or understand how your option’s premium might shift.