Greeks are tools used in options trading to measure different risks and help you understand how an option’s price might change. They show how factors like price moves, time, and volatility affect the value of your options. Knowing how Greeks work can give you an edge when making trading decisions.

Each Greek focuses on a specific part of the option’s behavior. For example, Delta tells you how much the option price will change if the stock price changes. Other Greeks like Theta measure time decay, while Vega tracks changes in volatility. Using these can help you manage your trades more precisely.

Learning how to apply Greeks can improve your trading strategies. You’ll know when to buy, sell, or hold your options based on the risks involved. This knowledge helps you control losses and maximize profits in options trading.

Core Principles of How Greeks Work

You need to know how different factors affect the price and risk of options. These factors help you measure the impact of price changes, time, volatility, and interest rates on your investments. Understanding them can improve how you manage options and make better trading decisions.

Understanding Delta and Its Impact

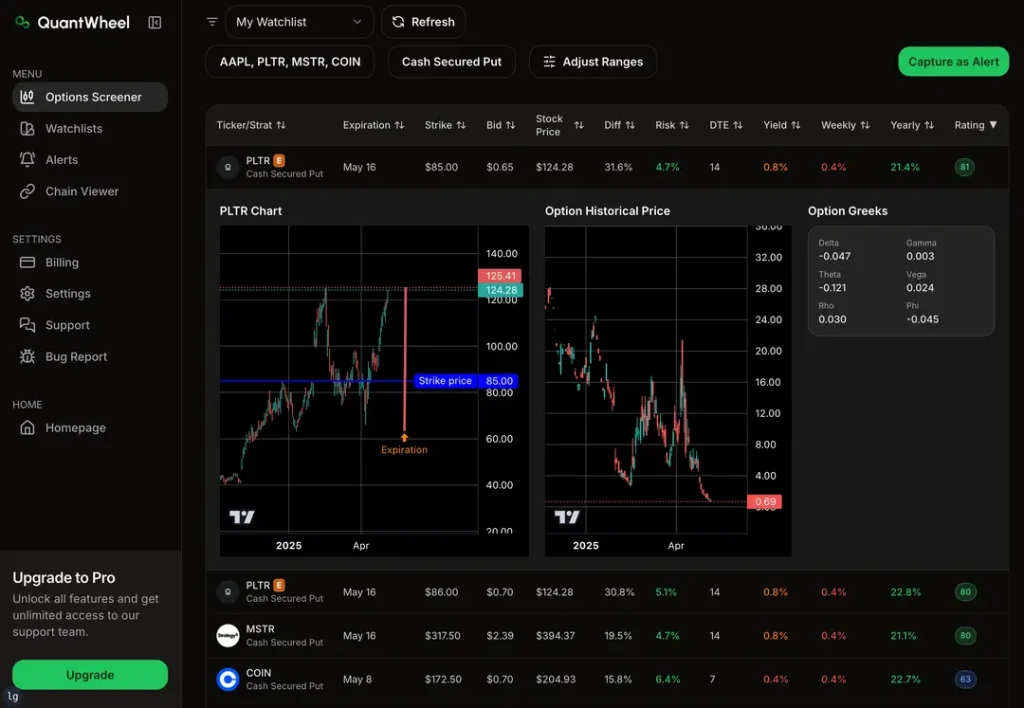

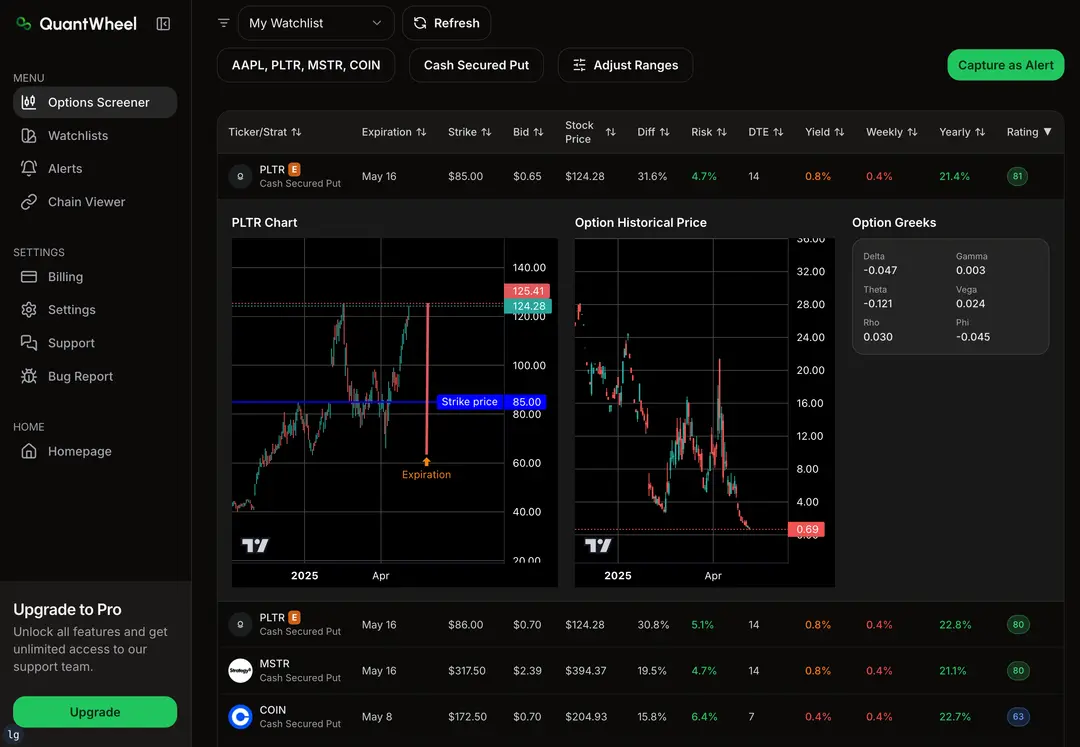

Delta shows how much an option’s price changes when the stock price moves by $1. If delta is 0.5, the option price will rise about 50 cents for every $1 increase in the stock price. Delta can be positive for calls and negative for puts.

Delta also tells you the chance an option will expire in the money. A delta close to 1 means a high chance; near 0 means a low chance. You use delta to hedge your portfolio by balancing stock and option risk.

Role of Gamma in Options

Gamma measures how fast delta changes when the stock price moves. When the stock price rises, gamma tells you how much delta will increase or decrease. High gamma means delta can change quickly, which makes your option more sensitive.

Gamma is highest for at-the-money options near expiration. It helps you understand risk as prices move. If you hold an option with high gamma, your risk and potential reward shift rapidly. Traders watch gamma to adjust hedges frequently.

Theta and the Effects of Time Decay

Theta measures how much value an option loses each day as it gets closer to expiration. This is called time decay. Theta is usually negative for option holders, meaning your option loses value every day without stock price moves.

Time decay speeds up as expiration nears. If you own options, theta works against you unless the stock price moves in your favor. Traders use theta to plan when to buy or sell, knowing the value will shrink just from time passing.

Vega and Volatility Sensitivity

Vega shows how much an option’s price changes when the volatility of the stock changes by 1%. Higher volatility usually means higher option prices since the chance of big moves increases.

Vega is larger for at-the-money options with longer time until expiration. If volatility rises, your option’s price goes up even if the stock price stays the same. You use vega to understand how market expectations about risk affect your option’s value.

Rho and Interest Rate Influence

Rho measures how much your option’s price changes when interest rates change by 1%. Call options usually increase in value as rates rise, while put options tend to decrease.

Interest rates don’t affect option prices much day to day, but they matter for longer-term options. If rates change, rho helps you estimate the effect on your option’s value. Traders use rho to plan around shifts in economic policies or market conditions.

Practical Applications and Strategies with Greeks

You use Greeks to better understand how options react to market changes. Knowing how they affect calls, puts, and your overall strategy helps you make smarter decisions. Greeks guide you in managing risk and improving your portfolio’s performance by measuring sensitivity to market moves.

Using Greeks in Options Trading Decisions

When you trade options, Greeks like Delta, Gamma, Theta, and Vega give key insights. Delta shows how much the option price moves as the underlying changes. For example, if Delta is 0.6, a $1 rise in the stock means the call option price increases by about $0.60.

Gamma tells you how Delta changes with the underlying price. Higher Gamma means more sensitivity, especially near the strike price. You watch Theta to understand time decay; it shows how much value the option loses each day if the stock doesn’t move.

Vega measures sensitivity to volatility changes. Increased volatility usually raises option prices. Using these Greeks, you can pick the right strike price and timing to fit your trading goals and market view.

Managing Risk and Portfolio Performance

Greeks help you control risk by measuring how your options respond to market moves. Delta allows you to hedge your positions by balancing positive and negative Deltas. This way, you reduce potential losses from price swings.

Theta warns you about time decay risk. If you hold long options, time will erode their value, so you may want to sell or adjust your positions before expiration. Vega controls exposure to volatility risk. You can reduce risk by shifting between options with different Vega levels.

By monitoring Greeks, you keep your portfolio stable. They guide adjustments to protect gains and limit losses when market conditions change.

Examples of Greek-Informed Strategies

You can use Delta-neutral strategies to limit risk by combining options and the underlying asset so that overall Delta is near zero.

This works well for traders expecting little price movement.

For income, sellers use strategies that benefit from Theta decay, like selling call options, making money as time passes without big price changes.

When expecting higher volatility, buying options with high Vega is smart.

For example, you might buy calls or puts before earnings announcements when big price moves are likely.

Using Greeks in these ways lets you build tailored strategies based on how your options respond to price, time, and volatility changes.