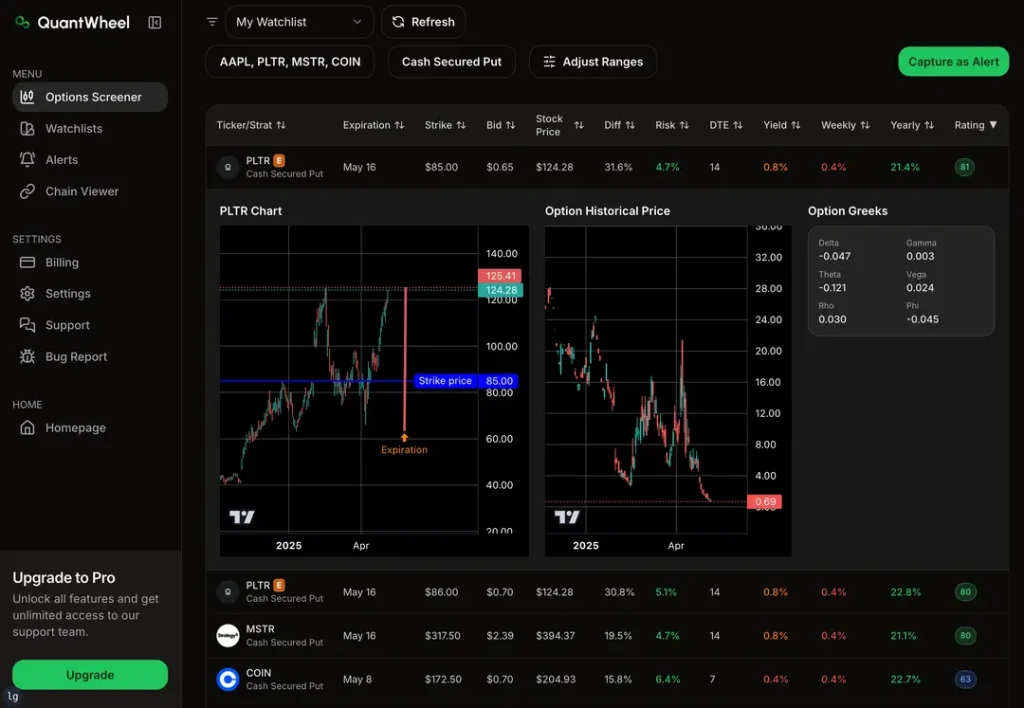

A cash secured put is an options strategy where you sell a put option while holding enough cash to buy the underlying stock if the option gets assigned. This strategy lets you earn income from the premium while potentially acquiring shares at a lower price.

Many investors use cash secured puts to generate steady income from their cash holdings. Instead of letting money sit idle in a savings account, you can put it to work by selling puts on stocks you want to own.

The strategy works best when you believe a stock’s price will stay flat or rise slightly. You keep the premium if the stock price stays above your strike price. If it falls below, you buy the shares at your chosen price using your reserved cash.

What are Cash Secured Puts?

A cash secured put is an options strategy where you sell put options while holding enough cash to buy the underlying stock if assigned. This strategy generates income through premium collection while potentially acquiring shares at a lower price.

Definition and Key Concepts

A cash secured put involves selling a put option contract while keeping enough cash in your account to purchase 100 shares of the underlying stock. When you sell the put, you receive a premium from the buyer.

The “cash secured” part means you have the full purchase amount ready. If you sell a put with a $50 strike price, you need $5,000 in cash per contract.

Key components include:

- Put option: Contract giving the buyer the right to sell shares to you

- Strike price: The price at which you agree to buy the stock

- Premium: Money you receive for selling the put

- Expiration date: When the contract ends

- Underlying security: The stock tied to the option

You become the seller of the put option. The buyer pays you premium for the right to sell you shares at the strike price before expiration.

How Cash Secured Puts Work

When you sell a cash secured put, you collect premium upfront. The buyer can exercise the option and sell you shares at the strike price anytime before expiration.

Two outcomes can happen:

- Option expires worthless: If the stock price stays above the strike price, the buyer won’t exercise. You keep the premium as profit.

- Assignment occurs: If the stock price falls below the strike price, the buyer may exercise. You must buy 100 shares at the strike price.

Your broker holds the cash as collateral during the trade. This cash cannot be used for other investments until the option expires or gets assigned.

Example: You sell a put option on XYZ stock with a $45 strike price for $2 premium. You need $4,500 cash secured. If XYZ stays above $45, you keep the $200 premium. If XYZ drops to $40, you buy shares at $45 but received $2 premium, making your cost basis $43 per share.

Benefits for Investors

Cash secured puts generate immediate income through premium collection. You receive this money upfront regardless of what happens to the stock price.

This strategy works well when you want to buy a stock but prefer a lower entry price. Instead of placing a limit order, you collect premium while waiting for the stock to reach your target price.

Income generation: Premiums provide regular returns on your cash holdings. This beats keeping money in low-yield savings accounts.

Lower cost basis: If assigned, your effective purchase price equals the strike price minus the premium received. This reduces your overall investment cost.

Flexibility: You can close the position early by buying back the put option. This allows you to take profits or cut losses before expiration.

The strategy works best in neutral to bullish market conditions. You profit when stocks move sideways or increase in value.

Risks and Considerations

Assignment risk: You must buy shares if the stock price falls below the strike price. This ties up your capital in a declining stock.

Opportunity cost: Your cash stays locked up as collateral. You cannot invest this money elsewhere while the position remains open.

Limited profit potential: Maximum profit equals the premium received. Even if the stock soars, you only keep the initial premium.

Market risk: If assigned shares in a bear market, you face potential losses if the stock continues falling. Your cost basis provides some protection, but losses remain possible.

Liquidity concerns: Some options have low trading volume. This makes it harder to close positions early at fair prices.

Consider your outlook on the underlying stock before selling puts. This strategy works best when you genuinely want to own the shares at the strike price. Avoid selling puts on stocks you wouldn’t want in your portfolio.

Implementing the Cash Secured Put Strategy

The implementation process requires four key steps, careful analysis of potential scenarios, active risk management, and understanding tax implications. Success depends on proper execution timing and maintaining adequate funds to cover your obligation.

Steps to Initiate a Cash Secured Put

First, select a stock you want to own at a lower price. Research the company’s financial health and recent stock price movements.

Next, calculate the cash amount needed. You need 100% of the purchase cost ready in your account. If you sell a put with a $50 strike price, you need $5,000 available.

Choose your strike price carefully. Pick a price below the current stock price where you feel comfortable buying the stock. Many investors choose strikes 5-10% below current market value.

Set your expiration date. Shorter periods like 30-45 days give you more control. Longer periods offer higher premium income but tie up your funds longer.

Place the put sell order through your broker. You receive the premium payment immediately. This premium is yours to keep regardless of the outcome.

Monitor your position daily. Watch how the stock price moves relative to your strike price. Track time decay as expiration approaches.

Example Scenarios and Results

Scenario 1: You sell a put on XYZ stock with a $45 strike price for $2 premium. Current stock price is $50.

If XYZ stays above $45 at expiration, you keep the $200 premium. The put expires worthless and you’re free to repeat the strategy.

If XYZ drops to $42 at expiration, you buy 100 shares at $45. Your actual cost basis becomes $43 per share ($45 minus $2 premium received).

Scenario 2: Market volatility increases after you sell the put. Higher volatility makes your put more valuable, creating a paper loss if you wanted to close early.

You can hold until expiration or buy back the put at a higher price. Buying back lets you avoid stock assignment but reduces your profit.

Maximizing Returns and Managing Risks

Select stocks with higher implied volatility to receive better premium income. Avoid stocks with upcoming earnings or events that could cause large price swings.

Diversify across multiple positions rather than putting all funds into one trade. This spreads your risk and provides steadier income.

Set profit targets for early closure. Many traders close puts when they capture 25-50% of the maximum profit potential.

Have a plan for assignment. Know exactly what you’ll do if you end up owning the stock. Consider selling covered calls as your next strategy.

Monitor your cash requirements carefully. Never sell more puts than your available cash can cover. Margin calls create forced liquidation at bad prices.

Track your annualized returns. Calculate your premium income as a percentage of cash used, then annualize based on holding period.

Tax Considerations and Costs

Premium income from selling puts counts as short-term capital gains. You pay ordinary income tax rates on these profits, not the lower capital gains rates.

If assigned stock, your cost basis equals the strike price minus premium received. This affects future tax calculations when you sell the shares.

Transaction costs reduce your net returns. Factor in commissions and fees when calculating potential profits. High-volume traders may qualify for lower commission rates.

Wash sale rules apply if you trade the same stock frequently. Losses may be deferred for tax purposes if you buy and sell similar positions within 30 days.

Consider holding periods carefully. Profits from puts held less than one year face higher tax rates than long-term investments.

Consult a tax professional about your specific situation. Complex strategies may create unexpected tax consequences that affect your overall investment returns.